VOE vs VOI vs VOIE: When Each One Matters in the Mortgage Workflow

VOE, VOI, VOIE—each verification type serves a distinct purpose. VOE confirms employment status, VOI confirms income, and VOIE confirms both in a single report.

In practice, those distinctions matter most when a platform fails to honor them: returning inconsistent data, routing incorrectly, or leaving operations teams to manually manage sequencing that should be automated. That’s where loan timelines slip and deals fall apart.

Lenders need a verification platform that can actually deliver the right type, at the right stage, for every borrower in the pipeline.

VOE: Verification of Employment

VOE confirms current employment status: job title, employer name, start date, and employment type (full-time, part-time, seasonal). It does not confirm income figures.

Lenders use VOE at application to establish basic eligibility and again at closing, where both Fannie Mae and Freddie Mac require re-verification, typically within ten business days of the note date.

Common methods:

- Direct employer contact via phone or written request

- Third-party database verification

- Payroll API integration

What can go wrong:

The most common VOE failure point is the human on the other end. Employers who don’t respond promptly, HR departments that have outsourced their VOE function to a third party, and small businesses with no formal verification process all add lag at exactly the wrong moment. Re-verification at closing has no timeline cushion, and delays here have a direct impact on close dates.

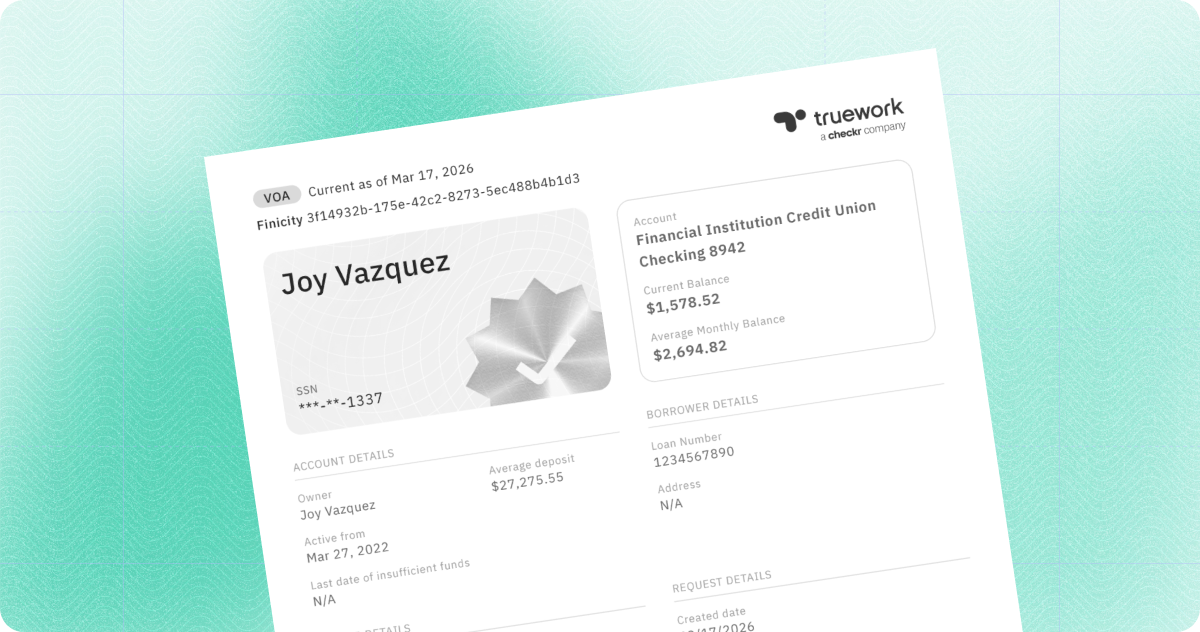

VOI: Verification of Income

VOI confirms the financial picture: gross income, pay frequency, year-to-date earnings, and any applicable bonus, overtime, or commission amounts. It does not confirm employment status.

Lenders rely on VOI throughout underwriting to calculate DTI, assess eligibility, and satisfy investor requirements. It also applies when employment has already been established via a prior VOE, but income details are still needed separately.

Common methods:

- Pay stubs and W2s (document collection)

- Tax transcripts via IRS Form 4506-C

- Payroll provider data via API or borrower-permissioned access

What can go wrong:

Data quality issues are most consequential here. Stale or inconsistent income figures can derail an otherwise complete file. Borrowers with multiple income sources, a salary plus freelance work, for example, may require separate verifications for each stream. And self-employed borrowers are where both problems converge: income is harder to verify quickly and typically requires multiple document types to tell a complete picture.

VOIE: Verification of Income and Employment

VOIE combines both VOE and VOI into a single report: one request, one reconciled data set, one deliverable for the file.

It’s the standard for GSE-supported automated underwriting and the default for lenders who want to reduce vendor touch points, eliminate redundant steps, and move loans through the pipeline faster.

What can go wrong:

Not all verification vendors that advertise VOIE actually deliver true VOIE. Some piece together a VOE result and a VOI result from different underlying sources without reconciling the data, which means lenders may receive a report that looks complete but contains inconsistencies that surface during underwriting.

The quality of VOIE varies considerably across platforms, and ‘we offer VOIE’ is not the same as ‘our VOIE data is accurate and consistent’.

Matching the Right Verification Type to the Right Moment

Knowing what each type confirms is one thing. The more operationally relevant question is when each one belongs in the pipeline, and for which borrowers.

The loan lifecycle has a predictable sequence: VOIE at pre-approval and underwriting to support the full file, and VOE re-verification close to closing to confirm nothing has changed. That sequencing is consistent across most loan types. What varies significantly is how that verification actually gets executed, because the right method depends on who the borrower is.

W2 employees represent the most straightforward case. A VOIE via payroll API or database verification is typically fast, accurate, and sufficient. Most lenders can handle this population at scale without much friction.

Self-employed and 1099 borrowers require more layered verification. Income can’t be confirmed through a single payroll source, so lenders typically need a combination: VOI via tax transcripts (IRS Form 4506-C) plus borrower-permissioned payroll data where available. This population is where verification timelines are most likely to extend.

Gig economy workers whose income flows through platforms like DoorDash or Uber were historically difficult to verify through traditional database methods. Consumer-permissioned verification that connects directly to gig platform accounts has changed that, enabling VOIE for a segment that previously created underwriting gaps.

Borrowers with multiple employers may require a separate VOE per employer, along with a combined VOI that aggregates income across all sources. This is one of the more complex scenarios operationally, and it’s where intelligent routing, rather than manual orchestration by the operations team, pays off most clearly.

The common thread? Sequencing the right report type for the right stage is table stakes. Matching the right method to the right borrower is where platforms actually differentiate. A verification platform that handles both automatically, without requiring the operations team to manage routing decisions, is a materially different tool than one that simply offers multiple methods and leaves the orchestration to the lender.

The Right Question Isn’t Which Type, It’s Whether Your Verification Platform Handles All Three

VOE, VOI, and VOIE each serve a distinct purpose in the mortgage workflow. The challenge for experienced lenders is to find a platform that consistently delivers the right type, with accurate data, at the right stage, for every borrower profile in the pipeline.

A platform that offers multiple verification types but requires manual management of when and how to deploy them shifts the operational burden back on the lender. A platform that handles orchestration automatically (routing by stage, method, and borrower type) doesn’t.

Truework’s one-stop verification platform combines instant payroll data, borrower-permissioned credentials, and Smart Outreach into a single workflow, covering VOE, VOI, and VOIE across virtually any borrower type, with intelligent routing that handles the sequencing so your team doesn’t have to.

See how Truework helps mortgage lenders reduce verification costs, improve completion rates, and close loans faster.