VOA in 2026: What’s Improved, What Still Creates Friction, and Why It Belongs Alongside Your VOIE Workflow

Mortgage operations teams have made real progress on income and employment verification over the last few years. Automated VOIE has become standard practice at most mid-to-large lenders, completion rates have improved, and costs have come down for teams that consolidated vendors.

Asset verification hasn’t kept pace. Not because the technology isn’t there: borrower-permissioned bank data connections have become reliable, GSE acceptance has expanded, and digital VOA has measurably reduced turnaround times for clean borrower profiles.

The gap here is structural. At most lenders, VOA still lives in a separate workflow and is managed by a separate vendor that underwriters reconcile manually with everything else. The mistake isn’t treating VOA as unimportant, but treating it as a standalone checklist item rather than a verification that should be sequenced and data-shared with income and employment. The result is a loan file that’s efficient on income and employment, and slow on assets.

The question is, why is VOA still creating friction, and what does it look like when it’s actually integrated?

What’s Actually Changed in the Last Few Years

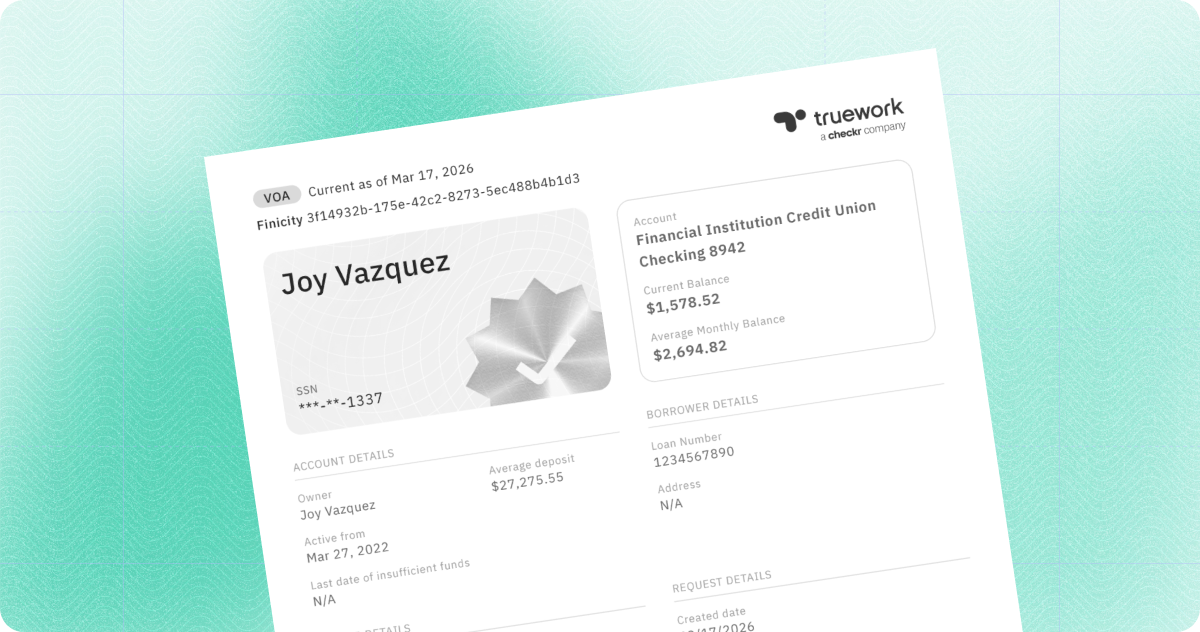

The shift toward borrower-permissioned bank data has been real and meaningful. Account aggregation through direct financial institution connections has replaced a significant portion of manual bank statement collection, cutting turnaround times, reducing document review burden, and producing more standardized, auditable records for underwriting.

The GSE policy environment has kept pace. As of September 2024, Fannie Mae expanded its Desktop Underwriter® (DU®) validation service to allow a supplemental deposit-based asset verification report to extend employment validation and satisfy the 10-day pre-close VOE requirement for eligible loans. Freddie Mac has similarly expanded Loan Product Advisor’s Asset and Income Modeler (AIM) to automate assessment of borrower assets, income, and employment, including income assessment using direct deposit data from asset account information.

For lenders who’ve built their workflows to take advantage of these rules, VOA now does more than it used to. A well-timed, well-connected asset report can eliminate a separate pre-close VOE order, reduce large deposit documentation requirements, and provide Fannie Mae Day 1 Certainty® on validated components, all from a single borrower authorization.

For lenders who haven’t, they’re paying for redundant reports and re-verification steps that current GSE guidelines don’t require.

The Friction That Still Exists

The benefits above are real. So is the gap between what digital VOA can do and what it actually delivers in most operational environments. The friction is less about the technology and more about how VOA is positioned in the workflow.

VOA sits outside the VOIE stack

At most lenders, income/employment and asset verification still come from different vendors, different integrations, and different report formats, which means different conditions, different review queues, and no shared data between them. A lender running VOIE through one platform and VOA through another is managing two vendor relationships, two data streams, and two points of potential failure on every file.

Large deposits still trigger manual review

Digital account aggregation doesn’t eliminate the need to source-document large deposits; it just makes the transaction history easier to pull. When an underwriter sees a $30,000 deposit from ‘Venmo’ or a wire transfer with no clear origin, the VOA report opens an investigation, not closes one. This is inherent to GSE guidelines, not a platform problem, but it’s worth naming as a consistent friction point regardless of how modern the tooling is.

Not all accounts connect cleanly

Smaller credit unions, certain investment platforms, and international accounts may not integrate with account aggregation providers, or may require borrower re-authentication partway through the process. Coverage claims from VOA vendors deserve scrutiny: ‘supports X financial institutions’ doesn’t tell you completion rates for borrowers who actually use those institutions.

Data inconsistency issues create delays

Joint ownership, account naming inconsistencies across institutions, and incomplete transaction histories still generate conditions, even on files where the borrower’s financial picture is clear. These conditions are disproportionately time-consuming relative to the actual underwriting risk they represent.

Re-verification at closing

Balance changes between initial VOA and closing can require a full re-pull, particularly when timelines stretch. This is a workflow design problem as much as a technology problem, and lenders who order VOA too early relative to closing create their own re-verification burden.

The Question Lenders Should Actually Be Asking

Most vendor conversations around VOA start with “Can you verify assets?” and “Do you support bank integrations?” Those aren’t the wrong questions, but they’re table stakes.

The questions that differentiate effective from ineffective VOA in 2026:

- How quickly can you produce a usable, underwriter-ready report? Not just access, usability. A report that generates immediately but requires manual conditions on 40% of files isn’t faster than a slower report that doesn’t. Completion rate and condition rate matter as much as turnaround time.

- How many borrower accounts can you actually access and complete? Coverage percentages for supported financial institutions are marketing numbers. Ask for completion rates on submitted requests, stratified by borrower type.

- Does this reduce conditions, or just change how they’re collected? Digital VOA that automates bank statement collection without reducing underwriting conditions hasn’t solved the problem. It has moved paper PDFs to digital ones.

- Does it eliminate steps from my workflow, or add another system to manage? A VOA vendor that requires a separate portal, a separate integration, and a separate reconciliation process has a high total cost of ownership regardless of per-report pricing.

Why VOA Belongs Alongside Your VOIE Workflow

The most meaningful operational shift isn’t about switching to a better VOA vendor. The aim is to collapse the distance between income/employment verification and asset verification so they share data, share a single borrower workflow, and feed into underwriting from the same platform.

The GSE policy environment now explicitly supports this. Fannie Mae and Freddie Mac have both expanded their verification frameworks to allow bank-data-based reports to support multiple verification needs, including income, employment, and asset validation from a single borrower-permissioned data source. Lenders who sequence VOA early and integrate it with VOIE can pull a richer borrower picture upfront, reduce downstream conditions, and eliminate re-verification steps that current guidelines no longer require.

The operational argument is also a data quality argument. When income, employment, and asset data come from disconnected vendors with different report formats, reconciling discrepancies falls on processors and underwriters. When they come from the same platform with shared borrower data, discrepancies surface earlier and resolve faster.

Truework now supports VOA alongside VOIE, unifying asset, income, and employment verification into a single workflow with intelligent orchestration across verification methods. For lenders who’ve consolidated VOIE but still manage VOA separately, that gap is worth closing. Digital VOA that isn’t integrated is just another system to manage. The distinction that actually moves the needle is whether your asset verification is connected to the same platform, the same borrower request, and the same workflow driving the rest of your pipeline.

Learn more about Truework’s VOA experience and how you can streamline your verification workflow.